달러는 당장 없어지지 않는다

위안화 결제 소식이 들리면서, 달러가 이제는 당장 세계 무역에서 물러날 거라는 얘기가 나오고 있습니다.

하지만 현실은 이 과정은 몇 세기에 걸쳐서 일어날 겁니다.

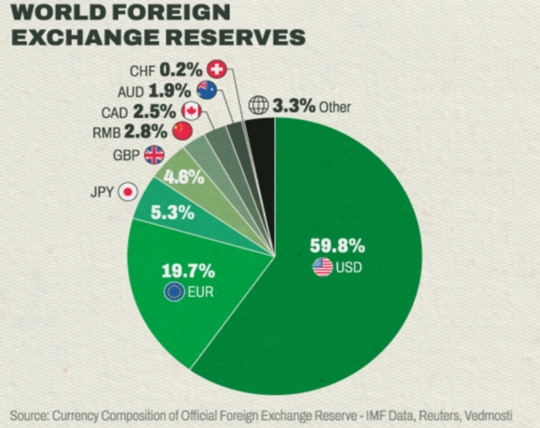

먼저, 달러는 세계 외환 보유고의 60%가 달러입니다.

시간에 따라서 외화 보유고 구성의 변화를 보면, 물론 달러의 비율이 "천천히" 감소하고 있습니다.

극적인 변화는 없습니다. 22년동안 대략 12% 감소했습니다.

호들갑 떨지 않아도 됩니다. 국가들은 달러 외의 통화를 가지고 거래할 수 있고, 하고 있습니다.

2019년에 달러로 표기된 부채는 인기가 제일 많았고, 지금도 그렇습니다.

그렇기에 FED가 다른 국가들의 중앙은행과 협업해서 달러 스왑 라인을 열어서 달러의 수요가 높을 때, 환율을 안정화시키려 하고 있습니다.

러시아가 우크라이나를 침공했을 때, 우리는 모두가 미국 달러를 향해 가는 걸 봤습니다.

아직도 달러는 '안전자산'이라는 생각이 있습니다.

왜냐하면 달러가 있으면, 미국 정부의 채권을 살 수 있고, 이 역시 '안전자산'입니다.

아래는 유로, 신흥국, 달러의 2010년 가격을 100으로 뒀을 때의 흐름무역 가중 달러 인덱스 또한 역시 다른 통화들에 비해 비교적 강세를 보이고 있습니다.

그리고 이건 어떤 상상을 해도 발상이 불가능한 사태가 임박했다고 보여주지 않습니다.

사실 반대죠

미국의 자산은 전세계적으로 인기가 많으며, 외국인들은 이 자산들의 큰 부분을 들고 있습니다.

이건 미국 달러에 대한 수요를 보여주며, 다른 통화나 결제 방식이 대체하기라도 할 때, 상당히 오랜 시간이 걸릴 걸 추측할 수 있습니다.

미국 정부채권에 대한 외국인들의 관심이 떨어졌지만, 중단기적으로 우려할만한 수준까지 내려간 건 아닙니다.

그리고 기준금리가 크게 상승했기 때문에, 외국인들의 관심은 다시 돌아올 수 있습니다.

유럽 밖에서 대부분의 세계 무역의 송장(Invoice)는 (놀랍게도) 미국 달러로 표기됩니다.

미국이 아닌 국가들이 아직도 미국 달러를 사용해서 무역을 하고 있기 때문에, 이런 관계와 상황이 급격하게 끝나진 않을 겁니다.

전세계의 부채 발행과 청구은 다른 통화보다도 달러를 통해 합니다.

전세계의 전체적인 통화 사용량을 보면, 달러의 수요는 꾸준히 있고, 그 다음은 유로입니다.

그리고 중국의 인민폐(Renminbi)는 잘 보이지도 않습니다.

현실은 가면 갈수록 더 많은 국가들이 유로보다는 달러로 결제를 하길 원하며 그 차이는 갈수록 커지고 있습니다.

이 모든게 가리키는 방향은 달러 패권주의의 몰락은 혹여나 발생하더라도, 아주, 아주, 아주 오래 걸릴 수 있습니다.

결론

세계 각국의 외환보유고에서 달러의 위치는 당장 변하지 않습니다.

달러의 패권이 끝난다는 소문은 20년째 들려오고 있으며, 저희는 맥락 없이 뽑아낸 수많은 뉴스 헤드라인을 봤습니다.

달러에 대해서는 패닉할 필요가 없습니다.

There's far too much talk around these parts about how the dollar will be vanishing from global trade imminently, but the reality is this is a process that takes decades.

First, the greenback makes up nearly 60% of global foreign exchange reserves. That's pretty massive!

In terms of currency composition of global foreign exchange reserves over time, yes the dollar has been *steadily* eroding.

Nothing dramatic here. About a drop of 12% over 22 years.

No need to panic. Countries can and do still trade outside of the US dollar!

As of 2019 the dollar was an extremely popular currency issue foreign debt in, and that remains the case now, which is why the Fed worked with other central banks to open forex swap lines to stabilize exchange rates during times of high demand.

When Russia's invasion of Ukraine occurred, we saw a flood into US dollars, as they remain seen as the 'safe haven currency'. That is because by buying dollars, one can also buy US government bonds, which are also seen as a safe haven. They caught a bid then as well.

The trade weighted US dollar index also remains quite strong relative to other trading partners' currency exchange rates.

That's not suggesting that there's some sort of imminent reckoning happening by any stretch of the imagination.

Quite the opposite, in fact.

US assets are also very popular globally, and foreigners hold a substantial portion of those same assets. That creates demand for the US dollar, as well as a much longer unwinding process should it ever be replaced by another currency or mechanism of settlement.

While the foreign appetite for US sovereign debt has diminished, it hasn't fallen to a point that warrants concern in the near to intermediate term.

And with rates having risen significantly, I suspect that appetite may begin to return.

Most global exports are invoiced in, you guessed it, US dollars outside of Europe.

These trade relationships, some of which are countries trading with each other (and not the US) in US dollars, are not likely to end abruptly.

Global claims and liabilities are much more likely to be settled in US dollars than other currencies (unlabeled charts above and below were sourced from the Federal Reserve)

In terms of overall international currency usage, the dollar remains rather robustly in demand, with the Euro the second most used, and a distant second. The Chinese renminbi is barely visible on the chart.

The reality is that more countries want to settle transactions and also finance debt using dollars rather than Euros, and the difference is rather significant.

This all suggests that any unraveling of dollar supremacy would take a very, very long time should it ever happen.

Conclusion: The dollar's role as the global reserve currency isn't changing anytime soon. There have been rumors about this situation for over two decades now, and we've seen numerous headlines taken out of context to mean things they do not.

There's no need to panic about the $

During an actual deflationary cycle, the dollar rallies hard. A meaningful credit crunch would actually support the dollar. I enjoy Reuters, but I think they lost some of the nuance in this headline about the moving parts underneath the surface...